It’s time for my semi-annual, or thereabouts, update on San Diego home valuations.

The idea is to measure the “expensiveness” of local housing by comparing home prices to their two most important fundamental underpinnings: incomes (how much people can afford to pay) and rents (how much it costs to put a non-owned roof over one’s head). This can be accomplished by creating a ratio between the typical home price and the typical income, or the typical home price and the typical rent.

It should be noted that these ratios combine data from many San Diego sub-markets that could be quite disparate in terms of price changes, rents, and residents’ incomes. So this is no magic formula — the ratios simply provide a very broad-brush look at whether the San Diego market in aggregate is cheap, expensive, or somewhere in between.

Let’s start with incomes:

The price-to-income ratio has continued the rise it kicked off in early 2009, but valuations by this measure aren’t looking too bad. While slightly above the long-term median, the price-to-income ratio is 17 percent below the 1979 and 1990 peaks. (I am using those two points in time as a comparison because they seem to suggest an upper limit from which home valuations had a hard time rising further in the absence of the manically reckless lending that marked this decade’s boom).

Things look a little richer according to the price-to-rent ratio. Valuations by this measure are well below those of the mid-2000s craze, but just 4 percent below the average level reached in the 1979 and 1990 peaks.

So while the price-to-income ratio indicates a market that is only slightly above normal valuation, the price-to-rent ratio suggests that San Diego homes are starting to get a bit spendy again.

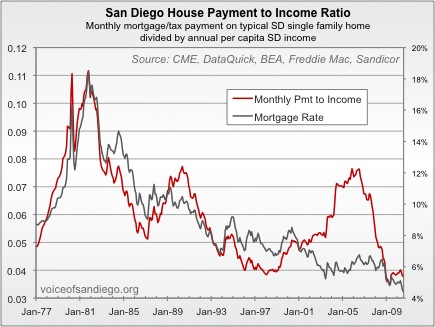

The boost in prices is no doubt partially due to the incredibly low mortgage rates currently available. The next two charts track monthly payment ratios, as opposed to purchase price ratios, and show that monthly payments are only slightly above their all-time lows.

The low monthly payments are no doubt luring renters off the fence. But as I’ve often discussed, when it comes to determining whether homes are overpriced on a sustainable basis it’s the price-based ratios that matter. Rates are low now and they are giving the market a boost, but that is a transient effect that lasts only as long as the low rates. If an individual buyer can lock in a low rate and stay in a home indefinitely, great — but how expensive homes are in comparison to their long-term fundamentals is a different question entirely, and one in which rates really aren’t relevant.

So we’ve got a serious mixed bag of signals. The payment ratios say homes are dirt cheap, but alas, that is the far less meaningful indicator. The more valuable price ratios are throwing off mixed signals — by their account, aggregate home prices are reasonable compared to incomes but flirting with overvaluation compared to rents. For an added dose of uncertainty about what valuation is “deserved,” consider the various economic factors at play: shadow inventory (yes, it’s a real thing) and the anemic job market on one side, and the potential for another round of government housing stimulus to spring to life on the other.

Things are as murky as ever, but at least this can be said with confidence: on the whole, San Diego housing is neither really expensive nor really cheap.

— RICH TOSCANO