The pot of money the San Diego Association of Governments relies on to pay for regional transportation projects is running low, and a liability caused by a 2005 financial deal gone bad is again rising and may worsen with news of a federal rate cut.

As Voice of San Diego first reported in 2017, SANDAG entered into three so-called interest-rate swaps, risky side deals tied to $600 million-worth of bonds sold in 2008 to pay for TransNet projects, like highways, trolley lines and habitat preservation.

With the swaps, SANDAG essentially bet interest rates would rise. When interest rates fell in the economic crash and stayed at historic lows, a multimillion-dollar liability appeared on SANDAG’s balance sheet.

The swaps are financial derivatives separate from normal bond debt payments backed by county sales tax revenue, which the agency is also having problems with.

SANDAG has repeatedly declared that the swap deals are working as intended, even though records show they’ve cost the agency at least $25.8 million to date.

As other public agencies benefit from low interest rates, and the increased borrowing power that comes with them, SANDAG loses on its 2005 swap deals. When rates drop, the liability gets bigger and SANDAG pays more.

Lots of other government agencies got out of losing swap deals when the market crashed, including San Diego County and the San Diego Metropolitan Transit System, but SANDAG kept the bulk of them.

SANDAG officials say there are no plans to change that. And doing so would be costly.

In 2005, SANDAG agreed to make normal debt payments with a variable interest rate to bondholders who provided $600 million in upfront cash in 2008 for regional TransNet projects. At the same time, SANDAG agreed to enter three swaps, whereby SANDAG would make separate, fixed-rate interest payments tied to the debt to Goldman Sachs, Bank of America and Merrill Lynch in exchange for a different, variable interest rate payment from those banks.

Got all that?

The two variable rates – one paid by SANDAG to bond holders, the other paid by large financial institutions to SANDAG – were supposed to cancel out, leaving SANDAG with just an attractive fixed rate loan. But that’s not how it has worked out. Under the deal, SANDAG has paid at least $4.2 million more to date than anticipated as of mid-2018, the agency’s 2018 financial statements show. SANDAG officials say that amount dropped to $3.24 million by the end of last fiscal year.

In 2012, SANDAG also paid $22.6 million to get out of a portion of the swaps using new debt that records show will cost $42.5 million to repay. That’s all money that could have gone to sorely needed transportation projects across the county.

Getting out of the rest of the swaps would now cost $85 million, as of this month, according to SANDAG. That’s the liability that remains and moves with the market. The negative value of that liability could be headed for another increase, with the Federal Reserve signaling Wednesday that it would cut rates to prop up a struggling economy. SANDAG officials were more optimistic, though, and said that may not happen.

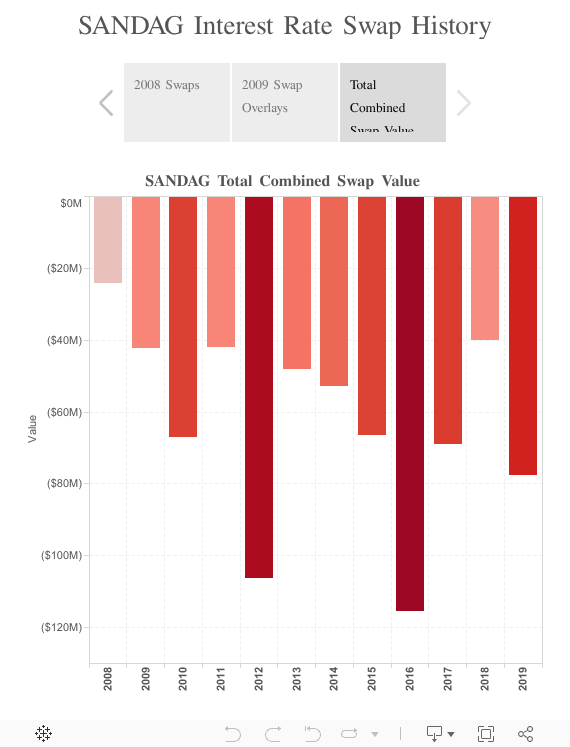

Records show the swap liability lessened in recent years as interest rates rose and the swap formula changed, but now with the return of low interest rates and an anticipated recession in the not-too-far-off future, SANDAG is moving further into the red once again.

SANDAG records show the swaps liability has fluctuated from $24 million to $115 million over the years, including a beneficial deal it entered into in 2009 that is helping to offset the damage.

But in the last 12 months, the swaps lost ground again – losing $51 million in value, SANDAG records show.

All told, SANDAG’s swaps were worth negative $77.6 million as of June 30, and negative $85.1 million as of Sept. 13, according to SANDAG officials.

“As long as the swap liability persists, it’s continued evidence of the bad bet they made before,” Lisa Washburn, managing director for the Massachusetts firm Municipal Market Analytics, who formerly worked at Moody’s Investors Service, told VOSD in 2017.

SANDAG officials – who are already coming to terms with a shortage of county tax revenue for planned projects – say TransNet is not suffering due to the swaps, and the liability doesn’t have to be paid since the swaps will remain until the 2008 debt is paid off in 2038.

What’s more, SANDAG doesn’t have to put up collateral for the liability, said SANDAG spokeswoman Jessica Gonzales.

But under the deal, SANDAG could be forced to pay up in full if certain credit ratings aren’t maintained by all swap parties, if SANDAG or the banks in the swap file for bankruptcy or if other requirements aren’t met. In other words, SANDAG’s claim that the liability is immaterial because they have no plan to get out of the deal is only true as long as the decision is left up to the agency.

A portion of the swap will also have to change soon, when an international market benchmark used in the deal is retired in 2021. It is unclear what impact that will have, and Gonzales said SANDAG officials are still working with their financial advisers, PFM Financial Advisors, to figure it out. The PFM team are also the ones who recommended the swaps to SANDAG in 2005, touting what great assets they’d become when interest rates rise, records show.

As for the repeated messaging by SANDAG officials that “the swaps continue to perform as expected,” Gonzales said that “refers to the fact that they are still providing a hedge against the variable rates bonds that were issued (in 2008). The fact that they are currently a liability is not what we are addressing by that statement.”

Low interest rates have been beneficial on other debt deals by SANDAG in recent years. Gonzales said bond debt deals in 2018 and 2019 achieved interest rates lower than 2 percent. SANDAG then invested the proceeds and earned more than 2 percent.

“These are real expenses and real interest rate earnings. The swaps are on paper and the gains/losses would not be realized unless sold. The decrease in rates has been positive for the debt program,” Gonzales said.